Private PMI signals China’s factories rebound as exports rally

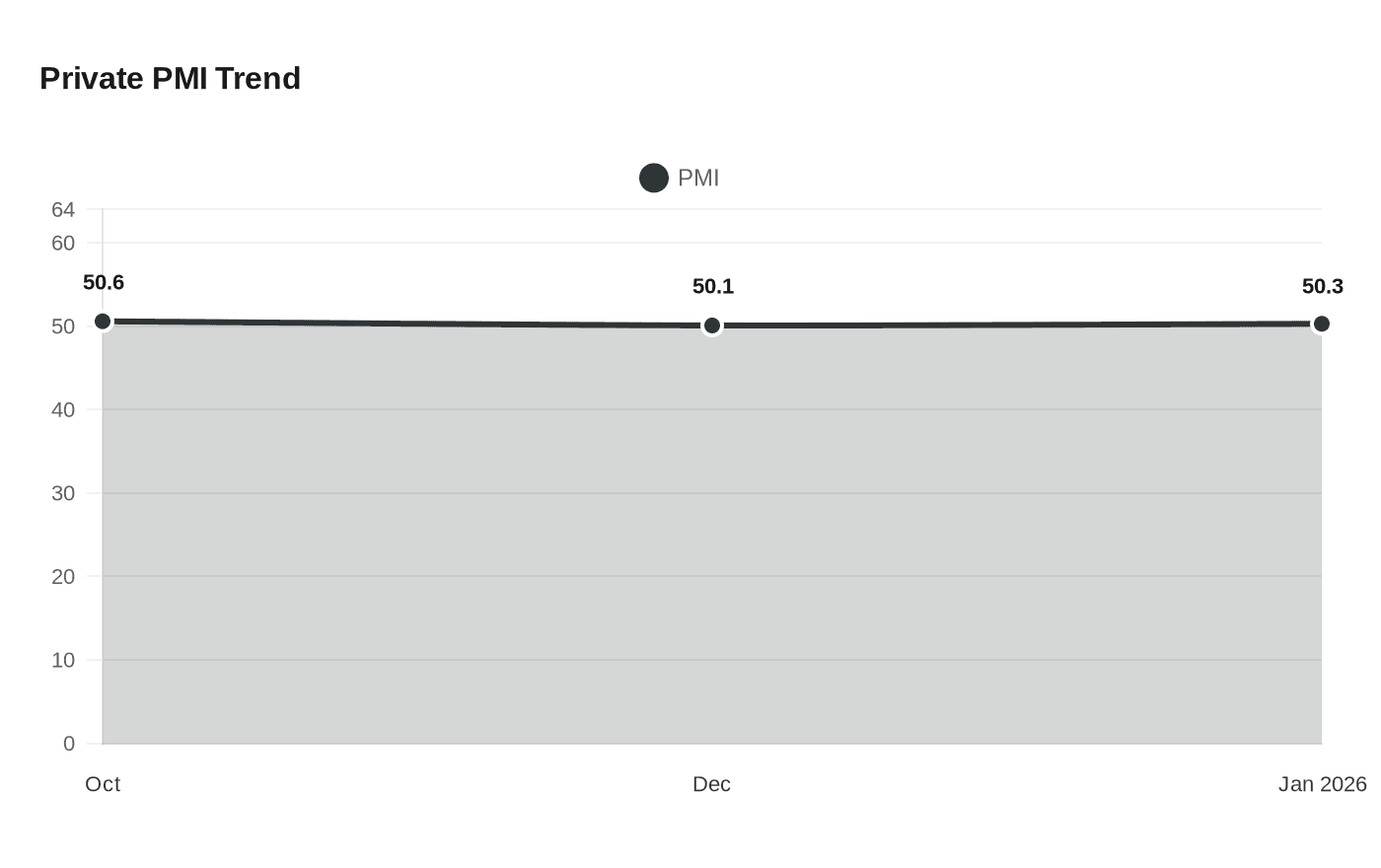

Private-sector PMI rose to 50.3 in January as export orders rebounded, suggesting export-led strength despite weak domestic demand and mixed official signals.

The private-sector manufacturing survey compiled by S&P Global showed a modest acceleration in China's factory activity in January, driven by a rebound in export orders and firms front-loading shipments ahead of the Lunar New Year.

"The seasonally-adjusted RatingDog China General Manufacturing PMI, conducted by S&P Global, rose to 50.3 in January from 50.1 the previous month, in line with analysts' expectations of 50.3 in a Reuters poll." A reading above 50 indicates expansion. That 50.3 print is the strongest private-survey result since October, when the index stood at 50.6, and marks continued, if cautious, momentum at the start of 2026.

"Manufacturers accelerated production and front-loaded cargoes ahead of the extended Lunar New Year holiday." The private survey said total new orders expanded for the eighth straight month, and new export orders rebounded, with demand particularly strong from Southeast Asia. Firms reported hiring rose to the highest level in three months as they coped with rising workloads and cleared outstanding orders.

Price dynamics were mixed. Corporate expenses expanded at the fastest rate in four months, pushing factory-gate prices up for the first time since November 2024. Metal prices, in particular, surged during the survey period, sending input cost inflation to its highest level since last September. At the same time business sentiment softened: the survey noted that "business confidence … slipped to a nine-month low, as firms worried about rising costs."

The private survey's upbeat trade signal contrasts with an official gauge published earlier that showed softer conditions. "That contrasts with an official PMI released on Saturday that showed factory activity faltered as orders deteriorated at home and abroad. Analysts said differences in survey coverage and respondent profiles likely contributed to the divergent readings." The gap highlights how sampling and respondent mixes can produce different snapshots of activity and complicates interpretation for policymakers and markets.

The rebound in exports helps explain why headline growth targets were met last year. Official figures show China's economy achieved the government's 5.0 percent growth target in 2025, underpinned by strong outbound shipments to non-U.S. markets even as slowing domestic demand and a property slump weighed on investment. Fixed-asset investment recorded its first annual decline in decades, contracting 3.8 percent, while retail sales slowed to their weakest pace in three years. Economists continue to flag persistent deflationary pressures as a downside risk.

For markets and policymakers the private PMI offers both reassurance and a warning. Export strength and higher factory-gate prices could support industrial earnings and narrow trade-driven disinflationary pressures, yet weak domestic demand and sliding confidence suggest any recovery remains fragile and narrowly based. Policymakers face a trade-off: the central bank and fiscal authorities may prefer targeted support for household income and demand while monitoring inflationary pockets tied to commodity prices.

In short, January's private PMI points to an export-led uptick in factory activity, but the broader recovery remains uneven. The next readings on domestic consumption, investment, and the official PMI will be critical to determine whether this export momentum can translate into a broader, sustainable industrial rebound.

Know something we missed? Have a correction or additional information?

Submit a Tip